Επικοινωνία

Επικοινωνία Πώς να κάνετε αγορές;

Πώς να κάνετε αγορές;Παράδοση

Οδηγός αγορών

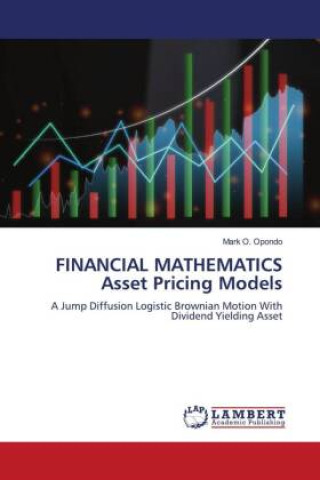

FINANCIAL MATHEMATICS Asset Pricing Models

Αγγλική

Αγγλική

145 b

145 b

30 ημέρες για την επιστροφή των προϊόντων

Μπορεί να σας ενδιαφέρει

/

Σκληρόδετη βιβλιοδεσία

/

Σκληρόδετη βιβλιοδεσία

83.43

€

83.43

€

Jump diffusion processes have been used in modern finance to capture discontinuous behavior in asset pricing. Pricing of assets in jump diffusions is consistent with the volatility smile often observed in financial markets. Logistic Brownian motion derived from logistic equation for asset security prices shows that naturally asset security prices would not usually shoot indefinitely (exponentially) due to the regulating factor that may limit the asset prices. Merton who was involved in the process of developing the Black-Scholes model came up with Merton jump model superimposed on Geometric Brownian motion. Therefore in this book, we have derived the price of dividend yielding asset that follows logistic Brownian motion with jump diffusion process and analyze the behavior of the derived model. This study used the knowledge of Geometric Brownian Motion and logistic Brownian motion, using the Heave-sides Cover-up Method we developed a price dynamic model. Data collected from Nairobi Security Exchange was analyzed to check the reliability of the formed.

Πληροφορίες για το βιβλίο

Αγγλική